Second letter to NBI Industrial Finance

Metrica today sent a second letter to the chairman of NBI: https://nbi-shareholders.com/2020/09/21/second-letter-to-nbi-board/

Metrica today sent a second letter to the chairman of NBI: https://nbi-shareholders.com/2020/09/21/second-letter-to-nbi-board/

Mr. LEE Hae-Jin

Chairman of the Board

LINE Corporation

JR Shinjuku Miraina Tower 23F

4-1-6 Shinjuku

Shinjuku-ku

Tokyo 160-0022

Japan

Dear Mr. Lee, (more…)

Bloomberg featured our views on the squeeze-out of LINE Corp shareholders (with no shareholder vote) by SoftBank Group and NAVER Corp.:

Metrica Partners Pte. Ltd. (“Metrica”) is the manager of, and adviser to multiple funds (the “Metrica funds”) that own shares in LINE Corp. (“LINE”, Securities Code: 3938). LINE is currently the subject of a tender offer (“the Joint Tender Offer”) by SoftBank Corp. (“SoftBank”, Securities Code: 9434) and NAVER Corporation (‘NAVER”, Securities Code: 035420), which is to be followed by a business integration with Z Holdings (Securities Code: 4689) (the “Business Integration”).

Metrica will not be tendering the shares held by the Metrica Funds into the Joint Tender Offer, and furthermore, it intends to dissent to the subsequent Share Consolidation and exercise its appraisal rights:

Metrica’s reasoning behind the above conclusions is as follows: (more…)

We have two situations which are public. The first is NBI Industrial Finance in India, a company which owns shares of a major listed cement company worth almost five times its market cap and which carries on almost no other business.

This month, we sent an open letter to the board which we also released to the press and uploaded to a dedicated website (link).

The letter was structured as a list of questions, in line with our policy of first seeking explanations for corporate behaviour before making our own suggestions.

In the first instance, we are asking: (more…)

SINGAPORE–(BUSINESS WIRE)–Metrica Partners Pte. Ltd. (“Metrica”) manages investment funds that are among the largest minority shareholders of NBI Industrial Finance Co. Ltd. (“NBI”, NSE: NBIFIN, Bloomberg: NBI IN).

NBI is a Shree Cement (“Shree”, NSE: SHREECEM, Bloomberg: SRCM IN) group company and shares its headquarters with Shree. According to Metrica’s research, almost 95% of NBI’s assets are represented by its holding in Shree and NBI has no debt. (more…)

Recent headlines such as “With M&A Hit, Wall Street Bankers Keep Busy With Stock Sales” (Bloomberg, 28 May), “Bankers fear sustained M&A slump: ‘It’s impossible without face-to-face meetings’” (Financial News, 8 June) and “Pandemic fears grip M&A as deal making slumps to 23-year low in Europe” (MarketWatch, 30 June) suggest a very depressed market for corporate transactions this year.

However, the numbers in Asia-Pacific tell a different story: (more…)

Metrica Partners is pleased to announce that assets under management have today risen to a record high, equivalent to more than thirteen times the level at which Metrica started three years ago.

The increase puts the business on a firm footing for long-term growth. Metrica would like to offer sincere thanks to everyone who worked hard throughout the various lock-downs to make this possible.

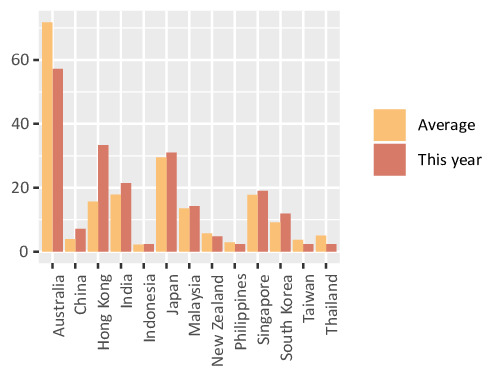

Transaction volumes continue to trend at high levels across the region. The chart below shows deal announcements this year (annualised) compared with the average since 2006:

One market stands out in particular: (more…)

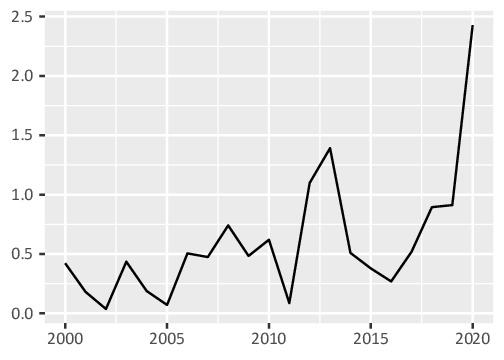

The figure below shows the cancellation / completion ratio of Asia-Pacific deals going back twenty years. The chart shows how this year has been a huge outlier, with the ratio moving well above two times, compared with a historical range rarely exceeding one. In other words, in 2020, more than two deals have been cancelled for every deal that has completed. This indicates the scale of the disruption in the M&A space this year.

M&A cancel / complete ratio (x)

What does this imply for M&A investment returns for the rest of the year? We think they will be strongly positive for the following reasons: (more…)