Vigilance is required

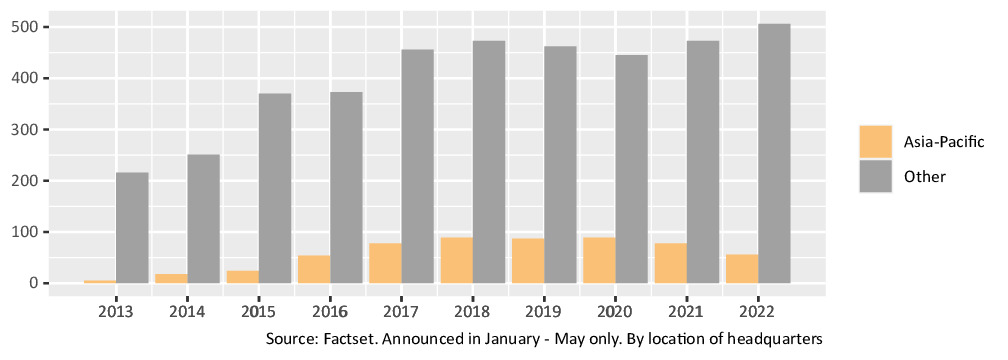

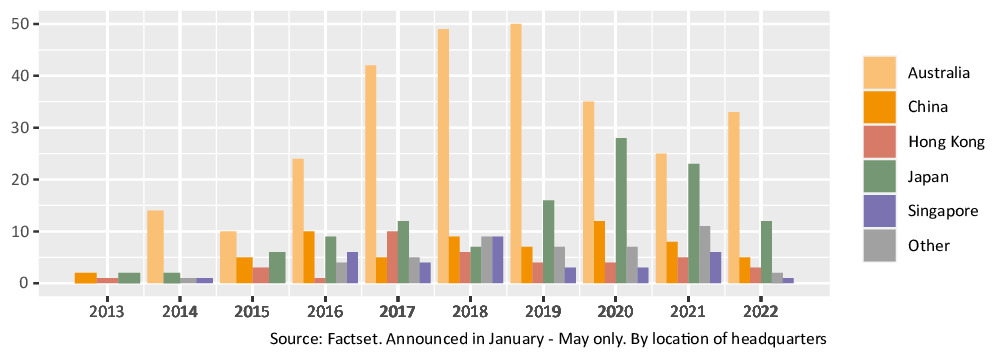

The start of the year has already brought five $100 million-plus Japanese takeovers, representing a decade-plus high for the month of January. It contrasts with a 36% year-on-year slowdown in global M&A. What is behind the uptick? (more…)